The Indian fintech landscape is experiencing a seismic shift, characterized by remarkable growth, evolving trends, and intricate regulatory developments. With over 2,000 recognized fintech startups operating across various sectors, India’s fintech ecosystem is set to become a juggernaut, with an estimated valuation of USD 150 billion by 2025. In this comprehensive exploration, we will dive into the multifaceted aspects of India’s fintech journey, encompassing the impact of COVID-19, emerging trends, the regulatory landscape, funding opportunities, and the vital realm of intellectual property (IP) protection.

The Impact of COVID-19 on Indian Fintech

Despite initial challenges posed by the COVID-19 pandemic, the Indian fintech landscape exhibited resilience and adaptability. Fintech companies swiftly harnessed digital solutions to meet evolving consumer needs. The pandemic accelerated digitization and financial inclusion efforts, resulting in an increased reliance on technology-driven financial services. As the world transitions back to normalcy, the question arises: how will this transformation impact the fintech industry’s trajectory?

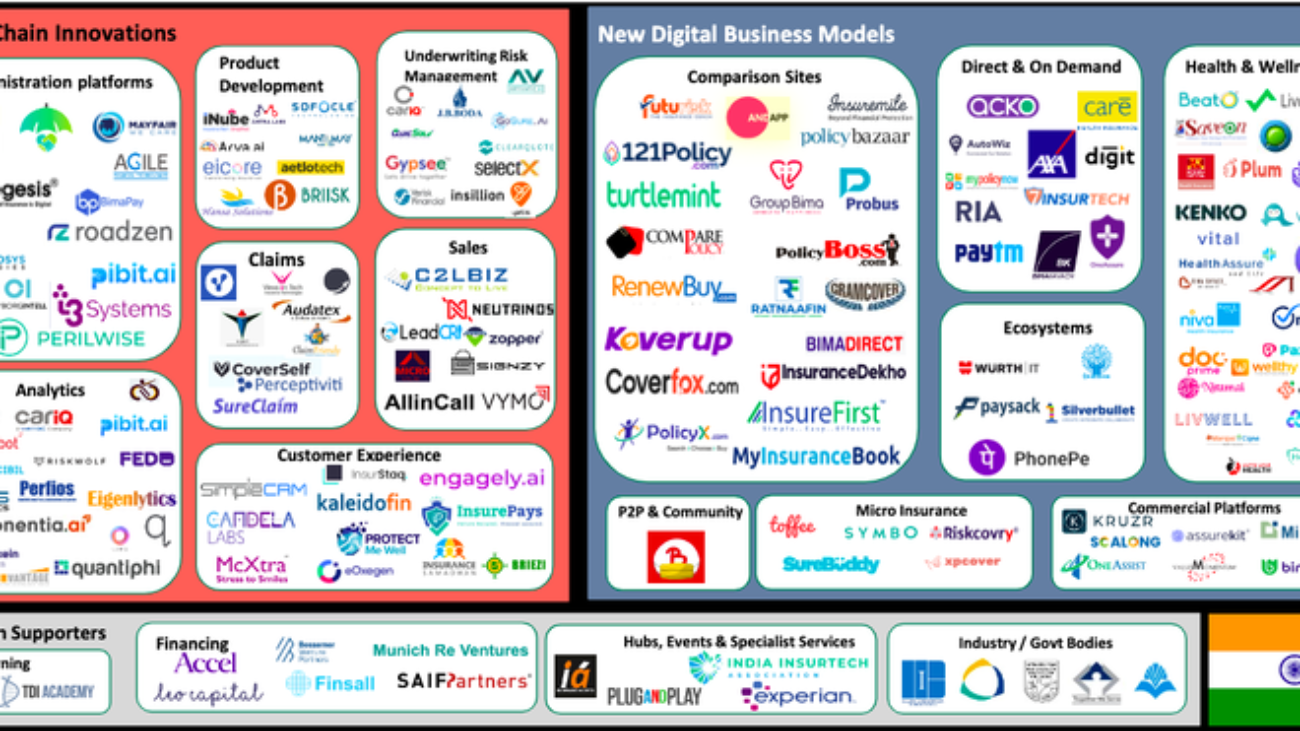

Emerging Trends in Indian Fintech

The Indian fintech landscape is a dynamic arena with several notable trends reshaping the financial landscape:

1. Buy Now, Pay Later (BNPL) and Micro-Credit: These solutions are gaining immense popularity among Indian consumers, offering flexible and convenient payment options.

2. Blockchain Technology: Blockchain is making significant strides in India, offering enhanced security and transparency in financial transactions.

3. Open Banking: Collaborations between fintech firms and traditional banks are on the rise, fostering innovation and customer-centric services.

4. Neo-Banks: Digital-only banks are disrupting traditional banking models, providing efficient and user-friendly financial services.

5. Embedded Finance: Financial services are seamlessly integrated into non-financial businesses, blurring the lines between fintech and tech companies.

6. Artificial Intelligence (AI): AI-powered solutions are streamlining operations and enhancing customer experiences in the fintech landscape.

7. Metaverse: The emergence of the metaverse is expected to impact fintech by enabling new forms of virtual transactions and digital assets.

8. Digital Payments: Digital payments continue to grow, with projections indicating that non-cash payments will dominate by 2026.

9. ESG Objectives: Environmental, Social, and Governance (ESG) objectives have gained prominence in the financial sector. Sustainable financing and ESG-linked products are on the rise, with regulators mandating ESG reporting for the top 1,000 listed companies. This trend reflects a growing commitment to responsible and ethical business practices.

Navigating the Regulatory Landscape

The regulatory environment for fintech businesses in India is multifaceted and evolving. The landscape is shaped by various regulatory authorities, including the Reserve Bank of India (RBI), Securities and Exchange Board of India (SEBI), Insurance Regulatory and Development Authority of India (IRDAI), Pension Fund Regulatory and Development Authority (PFRDA), and International Financial Services Centres Authority (IFSCA).

Regulated Fintech Activities: Fintech activities subject to regulation in India include online payments and transactions, payment aggregators and gateways, data protection, lending, securities trading, insurance offerings, and more. To engage in these activities, fintech firms often require prior approvals and licenses from the relevant regulatory authorities.

Cryptocurrency Regulation: India currently lacks dedicated regulation for cryptocurrencies or cryptoassets. The regulatory status of cryptocurrencies remains uncertain, with a draft bill proposing the creation of an official digital currency by the RBI and the potential prohibition of most private cryptocurrencies.

Regulatory Sandboxes: Regulatory authorities in India have introduced regulatory sandboxes, allowing fintech businesses to experiment with innovative solutions within controlled environments. The RBI, SEBI, IRDAI, and IFSCA offer sandbox options, enabling testing and refinement of fintech products and services.

Receptiveness of Regulators: Indian financial regulators and policymakers are increasingly open to fintech innovation aligned with existing regulatory structures. They emphasize the importance of customer protection, cybersecurity, financial integrity, and data protection. The establishment of institutions like the Reserve Bank Innovation Hub and collaborations with international counterparts underscore the commitment to fostering a thriving fintech ecosystem.

Challenges for Foreign Fintechs: Foreign fintech companies seeking entry into the Indian market may encounter challenges related to local presence requirements and foreign exchange control regulations. Compliance with data storage regulations, such as the RBI’s mandate for payment data to be stored within India, can pose difficulties for multinational corporations.

Funding Opportunities for Indian Fintechs

Indian fintech companies have access to a diverse range of funding options, including equity investments, debt financing, venture capital, and private equity. Additionally, government and state authorities offer incentives and schemes to support startups and growing businesses, further promoting investment and innovation within the fintech landscape.

IPO Conditions and Recent Revisions

To go public in India, companies must meet eligibility criteria set by the Securities and Exchange Board of India (SEBI). These criteria include profitability requirements, allocation to Qualified Institutional Buyers (QIBs), clean track records for promoters, and adherence to pricing guidelines. Recent revisions have made these requirements more stringent to reduce post-listing price volatility and enhance market integrity.

Navigating Intellectual Property (IP) Protection in India’s Fintech Landscape

In the rapidly evolving fintech sphere, the protection of innovations and inventions through IP rights is paramount. India offers robust IP protection mechanisms through legislation such as the Patents Act, Copyrights Act, Semiconductor Integrated Circuits Layout-Design Act, and Designs Act. The choice of protection depends on the nature of the fintech innovation, with patents suitable for technological solutions and copyrights safeguarding software code and creative content.

Ownership of IP: IP ownership is typically determined by contractual agreements. Clear and comprehensive contracts with employees, contractors, or partners are essential to define IP ownership and prevent disputes.

Exploiting and Monetizing IP: Fintech companies can monetize IP through licensing, outright sale, franchising, securitization, and other strategies. Licensing offers revenue generation without relinquishing ownership, while franchising enables expansion while retaining control over IP assets.

International Protection: India’s participation in international IP treaties allows for the protection of IP rights from signatory countries, facilitating global expansion for fintech companies.

Challenges and Considerations: Fintech businesses should be aware of challenges, such as the patentability of software, common law rights for trademarks, the importance of contractual clarity, and the potential need for legal enforcement of IP rights.

The Indian fintech landscape is a dynamic and promising industry poised for substantial growth. As fintech continues to reshape finance and technology, staying informed about regulatory developments, market trends, and IP protection will be crucial for both established players and newcomers in this vibrant ecosystem. With the right strategies and a keen understanding of the Indian fintech landscape, businesses can unlock the immense potential offered by one of the world’s most dynamic markets.